Key Finding

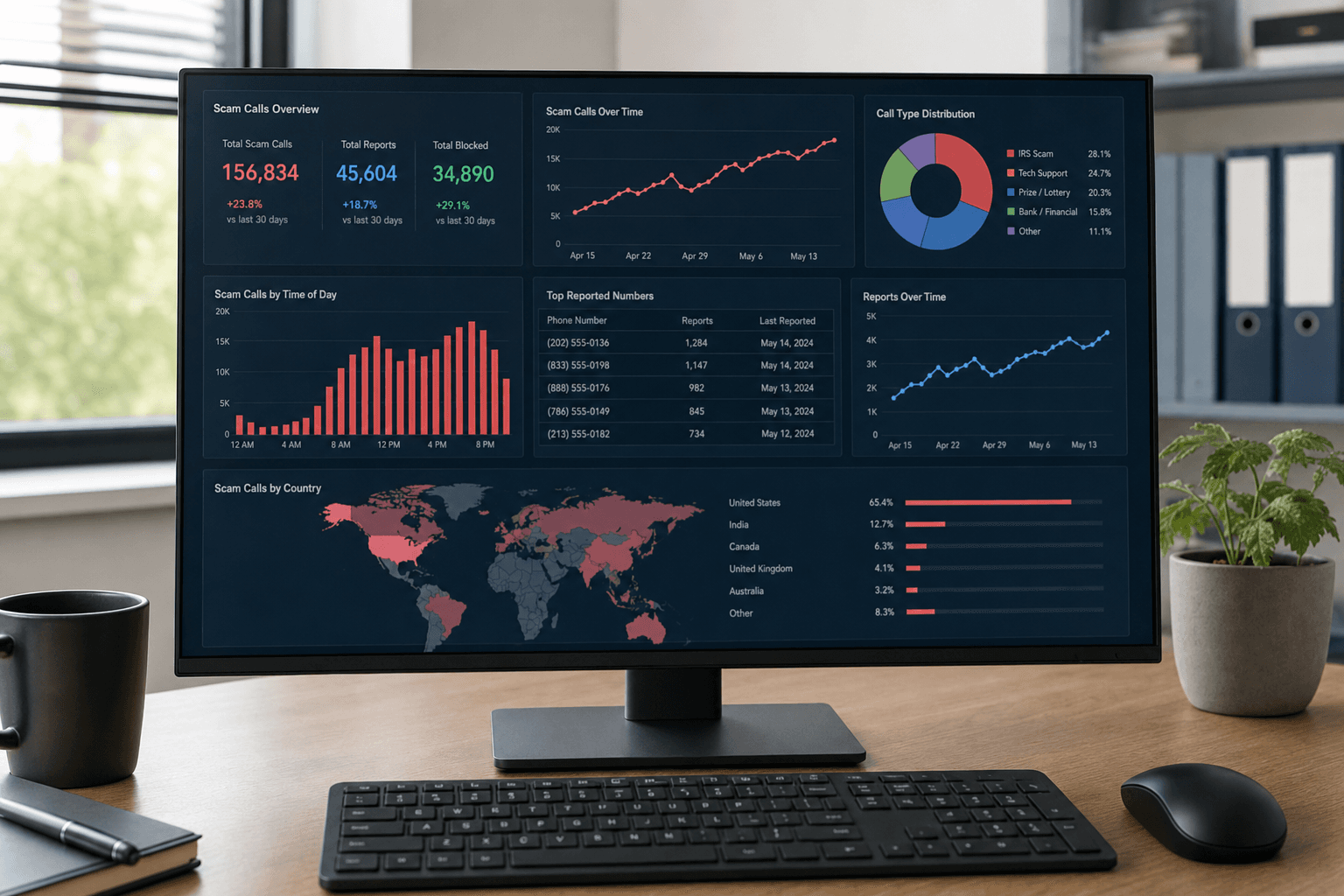

Debt-relief robocalls are not just America's most-complained-about phone scam. They are growing fast. ScamVerify™ data shows complaints about debt-relief calls jumped 79 percent in a single year, from 35,803 in May 2025 to 64,240 in May 2026. The robocall rate on these calls rose too, from 86 percent to 90 percent, meaning nine in ten of these calls are now pure automation. This report breaks down the surge and the simple rule that defeats every one of these calls.

The Numbers

| Metric | May 2025 | May 2026 | Change |

|---|---|---|---|

| Debt-relief complaints | 35,803 | 64,240 | +79% |

| Robocall rate | 86% | 90% | +4 points |

A 79 percent year-over-year jump in a category that was already the largest in the country is the headline. Debt relief now draws far more complaints than any other named scam type, nearly three times the next category, government and business impersonation. It sits squarely at the top of more than 15 million FTC complaint records in our database.

What a Debt-Relief Scam Call Sounds Like

The pitch is always a version of the same promise. A recorded voice claims it can:

- Slash your credit-card interest rate

- Settle your debt for "pennies on the dollar"

- "Forgive" your student loans through a special program

If you stay on the line or press a key, you are routed to a live closer who pressures you to pay an upfront fee, hand over your bank account or card number, or share personal details. The early payment or "enrollment fee" is the scam. The promised relief never comes.

Why It Keeps Growing

- It targets a real pain point. Millions of people carry credit-card, mortgage, and student-loan debt, so a promise to make it smaller lands on receptive ears in a way a fake lottery never could.

- It runs on automation. At a 90 percent robocall rate, these are dialers blasting recordings to massive lists and transferring only the people who engage.

- It rotates through numbers. Operations buy sequential toll-free numbers in blocks and rotate through them, so blocking one does little. We have tracked single numbers like 888-269-4978 grow to nearly 2,000 complaints, and entire prefix blocks carrying thousands more.

The Rule That Defeats It

Two facts from the Federal Trade Commission end every one of these calls:

- Legitimate debt-relief and credit-counseling services do not cold-call you with robocalls. A recording offering to fix your debt is a scam by default.

- Charging a fee before settling any debt is illegal. Any "enrollment," "processing," or "activation" fee demanded upfront is the scam revealing itself.

If a call asks you to pay before it does anything, hang up.

Red Flags

- A robocall or unexpected call offering to reduce, settle, or forgive your debt

- Pressure to "act now" before a fake deadline or "expiring program"

- A request for an upfront fee, your bank account, or your card number

- A demand for payment by gift card, wire, or cryptocurrency

- Instructions to press a key to "lower your rate" or "speak to a specialist"

What to Do

- Do not press any key. Pressing a number confirms your line is live and routes you to a closer. Hang up.

- Never pay upfront. No legitimate service charges before settling your debt.

- Check the number. Run any debt-relief caller through the ScamVerify phone lookup to see if it is already tied to complaints.

- Get real help safely. For genuine debt help, contact a nonprofit credit counselor you reach out to yourself, never one that called you.

- Report it to the FTC at ReportFraud.ftc.gov and DoNotCall.gov. Your report feeds the data that flags the next number.

The Bottom Line

Debt-relief robocalls were already the most-complained scam in the country, and they grew 79 percent in a year, now running at a 90 percent robocall rate. The operations exploit real financial stress and hide behind rotating toll-free numbers. The defense is simple and absolute: legitimate debt help never robocalls you and never charges before it delivers. Treat any unsolicited debt-relief call as a scam, never press a key, and look up the number before you trust it.

Check a debt-relief number now. Paste it into the ScamVerify phone lookup to see its complaint history.

FAQ

Are debt-relief robocalls a scam?

Almost always. The FTC is clear that legitimate debt-relief and credit-counseling services do not contact you through unsolicited robocalls, and it is illegal to charge a fee before actually settling a debt. ScamVerify data shows debt relief is the most-complained phone scam in the country, with a 90 percent robocall rate. Treat any recorded call offering to cut, settle, or forgive your debt as a scam.

Why am I suddenly getting more debt-relief calls?

Because the scam is surging. ScamVerify data shows debt-relief complaints jumped 79 percent year over year, from 35,803 in May 2025 to 64,240 in May 2026. The operations run on automated dialers and rotate through blocks of toll-free numbers, so even after you block one, near-identical calls keep coming from new numbers.

What happens if I press a key on a debt-relief robocall?

Pressing a key, even to "be removed from the list," confirms to the dialer that your number is active and a real person is listening. It typically transfers you to a live closer trained to pressure you into an upfront fee or into handing over bank details. The safest response is to not press anything and simply hang up.

How can I get legitimate help with my debt?

Reach out yourself to a reputable nonprofit credit-counseling agency rather than responding to any call, text, or email that contacts you first. Legitimate counselors will review your situation without demanding large upfront fees and without promising to erase your debt. If an offer arrives by robocall or pressures you to pay before doing anything, it is a scam.